Millennials, as a generation born between the early 1980s and late 1990s, encounter distinct financial challenges and opportunities in today’s rapidly changing economic landscape. With the right approach to financial planning, millennials can establish a solid foundation for long- term financial success. By understanding and implementing these principles, millennials can navigate their financial journey with confidence and build a brighter financial future.

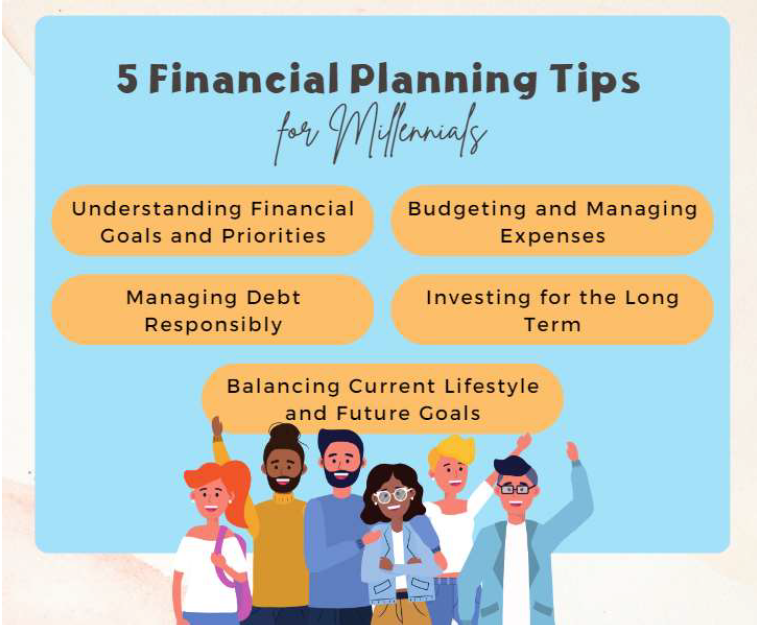

Understanding Financial Goals and Priorities:

Setting clear goals involves reflecting on personal aspirations, values, and desired outcomes. Millennials should consider their unique circumstances and identify specific financial milestones they wish to achieve. These goals may include saving for a down payment on a home, paying off student loans, establishing an emergency fund, or planning for retirement. By articulating these objectives, millennials gain a sense of purpose and direction in their financial journey.

Budgeting and Managing Expenses:

Budgeting is a cornerstone of effective financial planning, particularly for millennials navigating the complexities of modern economic landscapes. By diligently tracking their income and expenses, millennials gain a holistic view of their financial health, facilitating informed decision-making and long-term financial security. The process of creating a budget not only instills better control over spending habits but also enables the identification of potential saving opportunities. With a clear budget in place, millennials can adjust their financial priorities and allocate resources strategically, fostering a path to achieve their goals and aspirations. In this digital age, a wide array of user-friendly apps and online tools further simplifies the budgeting process, empowering millennials to take charge of their financial future with ease and confidence.

Managing Debt Responsibly:

Many millennials carry student loan debt and credit card balances. Managing debt responsibly is critical for financial success. It’s important to create a repayment plan, make regular payments on time, and consider strategies such as refinancing or consolidating loans to lower interest rates. By managing debt effectively, millennials can reduce financial stress and build a stronger financial future.

Investing for the Long Term:

Starting early and capitalizing on the power of compound interest can significantly boost their investment growth over the long term. Exploring low-cost index funds and exchange-traded funds (ETFs) offers diversified investment opportunities, helping millennials build a balanced portfolio. Engaging the services of a financial advisor can provide valuable insights, personalized guidance, and optimized investment strategies to make the most of their financial journey and secure a strong financial future.

Balancing Current Lifestyle and Future Goals:

Millennials often grapple with the intricate challenge of aligning their current lifestyle preferences with long-term financial aspirations. Successfully achieving a harmony between enjoying the present and saving for the future demands a thoughtful approach to spending, where needs take precedence over wants, and a willingness to embrace innovative money-saving strategies that don’t sacrifice their quality of life. By deftly navigating this equilibrium, millennials have the opportunity to lay the groundwork for a financially sustainable and rewarding future.

In conclusion, financial planning is a vital tool for millennials to achieve long-term financial success and security. By cultivating discipline, seeking ongoing financial education, and adopting a long-term mindset, millennials can confidently navigate their financial journey and lay the foundation for a prosperous future.

This article is for informational purposes only and should not be relied upon as financial advice.

General Advice Disclaimer

The information in this publication or any dissemination of information in any form is not intended to be and does not constitute financial advice, insurance advice or any other advice or recommendation of any sort offered or endorsed by finexis advisory Pte Ltd (“finexis”).

The information is not to be relied on as investment, legal, tax or other advice as it does not take into account the investment objectives, financial situation or particular needs of any specific investor.

Investment products are subject to investment risks including the possible loss of the principal amount invested. References may be made to past performance of investment products and it may not be indicative of future results. Buying insurance policy or investment product may require long-term commitment. An early termination of the policy or product usually involves high costs and the surrender value payable may be less than the total amount paid. Please refer to the relevant documents such as product summary or policy contract for the exact benefits and features.

If you need clarification, please do not hesitate to ask your financial consultant. You should not make any decision based on the information without undertaking independent due diligence and consultation with your financial consultant.

The information provided and / or this advertisement has not been reviewed by the Monetary Authority of Singapore.

Full disclaimer: https://www.finexis.com.sg/general-disclaimer.html